Managing AI Risks in Fintech: How to Avoid a $1M Non-Compliance Penalty

The fintech landscape has transitioned from an era of experimental curiosity to a period of mandated algorithmic core operations. By 2027, global spending on Artificial Intelligence (AI) in financial services is projected to reach $97 billion. Fintechs are gripped by an "action bias"—a strategic drive to innovate that often outperforms internal governance.

However, as innovation accelerates, so does the risk. Corporate transparency data shows a staggering shift: in 2023, only 12% of S&P 500 companies identified AI as a material risk in their public disclosures. Today, that number has exploded to 72%.

The Big Problem: the Limitation of AI Risk Visibility

For the modern CISO or Compliance Officer, the biggest challenge isn't the AI itself; it's the lack of visibility into the "Black Box." Many fintechs are deploying high-stakes models for credit scoring, fraud detection, and autonomous trading without a way to audit the "why" behind an algorithmic decision.

In this new regulatory climate, the liability has shifted. If a model behaves in a discriminatory way or triggers a data breach, the regulators aren't looking for the developer—they are looking for the CISO. When an algorithm fails or leaks sensitive financial credentials, the resulting legal and reputational costs can define a firm’s future valuation.

Traditional financial controls were built for a slower world. For decades, audit protocols like Sarbanes-Oxley (SOX) relied on "manual sampling"—testing maybe 1,000 transactions out of a million. In an AI-first world where bots execute billions of operations 24/7, manual sampling is no longer secure; it’s a gamble.

To survive 2026-era scrutiny, fintechs must transition from episodic audits to Continuous AI Monitoring. This isn't just about catching hackers; it’s about maintaining "conceptual soundness" across your entire digital stack. Similar to the [healthcare data sovereignty paradox]([healthcare data sovereignty paradox](https://www.langprotect.com/blog/ai-chatbots-security-risk-in-healthcareLink Text))—where AI must be used but data must be protected—fintechs must now figure out how to satisfy global regulators without hitting the "kill-switch" on innovation.

In this pillar report, we will deconstruct how to bridge the gap between AI speed and regulatory safety using a "governance-first" architecture.

Deconstructing the Modern Fintech Risk Profile

In the financial sector, AI risks are not merely technical bugs; they are strategic liabilities. As fintechs transition toward autonomous operations, the "attack surface" is moving from simple software vulnerabilities to the very logic of the algorithm itself. To protect your firm, you must recognize that AI risk is now multi-dimensional.

The Conceptual Soundness Gap: When Design Becomes a Liability

The most expensive failure in fintech AI is often "Conceptual Failure"—when a model works exactly as programmed, but the program itself is fundamentally flawed or biased. Unlike a server crash, these failures are silent, growing inside your system until a regulator intervenes.

A prime example is Earnest Operations' $2.5 million settlement. Their lending models were found to contain embedded biases that led to discriminatory outcomes. This wasn't a "hack" in the traditional sense; it was a failure of the algorithm's reasoning logic.

For fintechs, this highlights a critical need for Explainable AI (XAI). If your model cannot explain why it rejected a loan or flagged a transaction, you are carrying a "black-box" liability that could result in brand-defining legal penalties.

Cybersecurity Multipliers: The Era of AI-Powered Vishing

While internal bias is a design risk, external threats have evolved into Cybersecurity Multipliers. Adversaries are now using GenAI to automate attacks that used to require massive human effort.

- Deepfakes and Vishing: Hackers are using high-fidelity voice cloning (Vishing) and deepfake video to bypass traditional Multi-Factor Authentication (MFA). Imagine a bot that calls your support desk, perfectly mimicking the voice of your CEO, to authorize a high-value transfer.

- Prompt-Driven Intrusions: Bad actors are utilizing prompt injection techniques to "trick" financial assistants into revealing proprietary secrets or environmental variables.

These aren't future threats; they are happening now. As hackers use AI to move at "machine speed," legacy defenses like static firewalls fail. You need a security layer like LangProtect Armor that can detect the semantic intent behind these interactions before the breach is finalized.

Comparison: The Scaling Risk Profile (2023 vs. 2026)

To visualize the shift in institutional risk, we must look at the data trends across the three main pillars of financial integrity:

| Risk Category | 2023 (Experimental AI) | 2026 Profile (Autonomous AI) | Why It Matters |

|---|---|---|---|

| Reputational | 12% Coverage: Focus on PR blunders and “odd” chatbot answers. | 38% Coverage: Massive erosion of trust due to algorithmic bias and unclear logic. | Brand trust is the bedrock of customer retention in banking. |

| Legal / Regulatory | 15% Coverage: Generic privacy concerns and simple data logs. | 41% Coverage: EU AI Act compliance, GDPR Article 22, and SOX scrutiny. | Non-compliance now carries $100M+ potential penalty weight. |

| Cybersecurity | 10% Coverage: Simple phishing and basic malware attempts. | 20% Coverage: Automated vishing, deepfakes, and promptware. | The attack surface has moved from the network to the intent. |

| Operational | 8% Coverage: Manual model validation every quarter. | 24% Coverage: Systemic dependency on unmonitored “black box” providers. | Model drift can trigger cascading financial failures in minutes. |

The Bottom Line for Leadership

This shift indicates that the fintech industry can no longer rely on occasional security check-ups. The goal must be to secure the "Invisible Workforce." Whether it is a loan officer using an unmanaged browser extension or a sophisticated RAG-poisoning attempt on your vector database, you must move from "Locking the door" to "Governing the Interaction."

As we have seen in our analysis of why banning ChatGPT creates more Shadow AI risk, the only path forward is through visibility. Only with a unified governance tool like LangProtect Guardia can a firm monitor its autonomous agent identities and ensure that algorithmic innovation remains an engine for growth rather than a source of liability.

Can AI Improve SOX Compliance? Shifting to Total Population Analysis

In the traditional finance world, auditing has always been a game of "searching for a needle in a haystack." Under Sarbanes-Oxley (SOX) requirements, teams would manually pick a few hundred transactions to test, hoping they represent the health of the entire company. In 2026, this "sampling" method is no longer a defense—it’s a liability.

Why Manual Sampling is a Legacy Failure

Standard auditing protocols usually involve testing roughly 1,400 manual journal entries (MJEs) per year. While that sounds like a lot, a modern fintech or digital bank processes millions of transactions every single day.

Manually checking a fraction of 1% of your data is like trying to protect a massive waterfall by checking a few drops of water with a magnifying glass. If an error or a fraudulent entry occurs in the other 99.9% of your data, you are completely blind to it. This "Visibility Gap" is exactly where material misstatements and regulatory fines hide.

The Solution: Satisfying AS 2401 with AI

To achieve modern compliance, fintechs are moving toward Total Population Analysis (TPA). Instead of testing a small sample, AI-driven auditing tools scan 100% of the General Ledger. This shift is critical for satisfying Auditing Standard (AS) 2401, which focuses on a firm’s responsibility to detect fraud.

- 100% Visibility: AI can review every single interaction between vendors and accounts.

- Unsupervised Risk Scoring: Instead of looking for a specific mistake, the AI learns what "normal" looks like. It then flags any interaction that is rare or suspicious, even if that mistake hasn't happened before.

Real Impact: From Months of Labor to Instant Results

The efficiency gains of moving from manual to autonomous auditing are transformative for the bottom line. Consider this real-world example of a firm that updated its reporting stack:

- Before AI: The team could only manually review 1,400 entries per year.

- **With AI-Driven TPA:**They instantly analyzed 300,000 transactions.

- The Outcome: The system identified high-risk anomalies across billions in assets that would have been missed by human eyes—while simultaneously saving over 350 hours of supervisor review time.

Common Question: Is my audit team safe?

The Problem: Even though AI improves the audit, it creates a new "side-door" risk. If your compliance officers or auditors start using unmanaged Shadow AI tools to help summarize these reports, they may accidentally paste sensitive financial credentials or company strategy into a public model.

The Fix: When scaling your SOX protocols with AI, you must use a tool like LangProtect Guardia. It ensures that your "Human-in-the-Loop" remains secure by monitoring and preventing secret and credential leaks during the auditing process.

CISO Implementation Tip:

To move toward Total Population Analysis, don't just "bolt on" an AI tool. Use interaction-aware governance to make sure that the people managing your millions of transactions aren't the ones unknowingly leaking the data that the AI is trying to protect.

Managing Fairness: How the "0.8 Rule" Protects Algorithmic Integrity

In the world of Fintech, the algorithm is often the final judge of who gets a loan, a mortgage, or a credit line. However, a model can be highly accurate but still legally toxic. For a Fintech firm to be truly defensible, it must solve the problem of "Disparate Impact."

Detecting Hidden Bias: The 80% Rule

Federal regulators (under the Equal Credit Opportunity Act and the Fair Credit Reporting Act) often utilize the "Four-Fifths Rule" (the 0.8 ratio) as a standard to detect bias.

- The Math: If the approval rate for a protected class (based on race, gender, or age) is less than 80% (0.8) of the rate for the highest-performing group, the system is flagged for "adverse impact."

- The Risk: Deep learning models are excellent at finding "proxy variables." Even if you remove "race" or "gender" from your data, a model might "learn" to discriminate by looking at zip codes, educational history, or even specific shopping habits.

If your Fintech doesn't proactively monitor this ratio, you are operating with a massive regulatory liability that could trigger fines reaching into the millions.

Strategic Fix: Pruning for Fairness

To stay compliant with the FCRA, developers shouldn't just "let the model learn." You must practice Feature Selection Pruning. This involves identifying specific variables that are contributing to biased outcomes and either removing them or "dampening" their weight within the model’s logic.

- Audit-Ready Models: LangProtect’s Breachers Red stress-tests your lending models by simulating diverse demographic prompts. It finds where the 0.8 ratio is being breached before you ship the model.

- Shadow AI Conflict: A critical point often overlooked is that banning sanctioned AI tools in Fintech actually makes bias worse. When employees use unmonitored "subterranean" AI tools to help make manual credit overrides, that activity is invisible to your compliance engine. You lose the ability to prove that bias didn't enter the loop via unmanaged browser extensions.

To ensure your team stays ahead of the coming regulatory crackdown, we have developed this 10-point readiness checklist. If you cannot check all ten boxes, your Fintech firm may be carrying a "hidden" compliance liability that could lead to six- or seven-figure fines.

The Fintech AI Compliance Checklist: 10 Essentials for Security Teams

This checklist is designed to align with the latest mandates from PCI DSS 4.0, SOX, and the EU AI Act.

Identity Inventory (NHI): Have you cataloged every "Non-Human Identity" (AI agent or bot) that has access to your production database?

The 0.8 Bias Threshold: Do you have an automated alert system that triggers if the approval rate for any protected class falls below 80% of the highest-performing group?

Real-Time Prompt Injection Defense: Is there an active firewall like Armor scanning financial instructions at the semantic level before the model processes them?

Shadow AI Discovery: Have you scanned your network to find unmanaged AI browser extensions being used by traders, loan officers, or clerks?

Audit-Ready Explanation (XAI): For every loan rejection or credit score change, can your team generate an automated SHAP or LIME report to satisfy GDPR Article 22?

Immutable Logic Logs: Are your "AI Reasoning Traces" (the thoughts behind the model's output) stored in a cryptographically secured, 6-year retention ledger for federal auditors?

Least-Privilege Agent Access: Does your "Billing Agent" have access to your "Customer Support" logs? (The answer should be no; agents should have strictly partitioned access).

Automated PHI/PII Redaction: Is there a layer like Guardia redacting credit card numbers and medical info before an employee pastes them into a public chatbot?

Continuous Stress Testing: Do you run weekly adversarial attacks using automated Red Teaming to find logic holes in your lending models?

The Human Override: Is there a hard "kill-switch" and a manual oversight protocol for any AI-driven transaction over a specific dollar amount?

Taking the Next Step: Your Roadmap to Algorithmic Resilience

Fintech growth is no longer just about building a faster model; it is about building a defensible model.

In the high-velocity world of financial services, you cannot rely on annual check-ups or manual sampling to keep you safe. The complexity of agentic AI risks and the move toward Total Population Analysis requires an automated governance plane.

By implementing these 10 steps, you transform compliance from a "Business Bottleneck" into a Competitive Advantage. While your competitors are busy answering for their bias settlements or data breaches, your firm will be leading with transparency and total integrity.

The Billion-Dollar Opportunity

According to BCG, banks and Fintechs that adopt AI-driven Interaction Governance achieve a 30% reduction in regulatory time-to-market. Don't let your innovation become a source of systemic liability.

Ready to Secure Your Fintech AI?

Whether you are trying to solve data leaks in cloud AI or hardening your hospital medical agents, LangProtect provides the interaction firewall the finance industry demands.

Take the first step toward a zero-incident audit.

Operationalizing Trust: Your 4-Step Strategic Roadmap with LangProtect

For Fintech leaders, the goal isn't just to "protect" data; it is to operationalize trust. You need a system that acts as the "Steering Wheel" for your AI innovation. To move from a risky, unmanaged environment to a fully governed clinical-grade financial operation, we utilize the LangProtect framework.

Here is how LangProtect secures your fintech's future in four actionable steps.

Step 1: Inventory the NHI Workforce (Cataloging Every AI Agent)

You cannot govern what you do not see. In most fintechs, there is a hidden army of Non-Human Identities (NHI)—autonomous browser extensions, unmanaged ChatGPT accounts, and small internal "wrappers" built by different teams.

- The Action: Use LangProtect Guardia to perform a full discovery sweep of your organization.

- The Win: This creates an "Identity Inventory," exposing unmanaged Shadow AI sprawl and cataloging every bot currently interacting with your sensitive data. By giving every bot a "Security Clearance," you eliminate the "Invisible Insider" risk.

Step 2: Bridge Legacy Data Silos (Securing Agentic Reasoning)

Most financial firms are a "Brownfield" environment—they are a sea of legacy databases and fragmented APIs. When you connect an AI agent to these silos to generate medical or financial reports, the risk of data exfiltration and "Over-Retrieval" is massive.

-

The Action: Move toward real-time, governed data feeds for your agentic systems.

-

The Win: LangProtect ensures that when an agent reaches into an old core-banking system or EHR database, the interaction follows strict context-aware policies. You ensure that a "summarization bot" never sees data it isn't authorized to touch, effectively satisfying the HIPAA and GDPR Minimum Necessary Standards.

Step 3: Secure the Cloud Interaction (Armor the Pipeline)

Fintech is increasingly cloud-first. Whether you are using OpenAI, Amazon Bedrock, or your own private cloud LLM, the "Prompt" is your new attack surface. If a hacker sends a malicious prompt, your cloud firewall won't stop it, but LangProtect Armor will.

- The Action: Deploy LangProtect Armor as a dedicated "interaction layer" between your users and your Cloud-AI data pipeline.

- The Win: Armor intercepts every prompt in under 50ms, scanning for semantic intent and injection attacks. This creates a Fortified Pipeline where financial data can move at the speed of the cloud while remaining under the lock and key of a specialized financial firewall.

Step 4: Continuous Behavioral Auditing (Staying Regulation-Ready)

The biggest liability in AI is "Model Drift"—where the AI's logic decays over time, leading to bias or logic errors. In a world where 72% of companies identify AI as a material risk, manual annual check-ups are no longer sufficient.

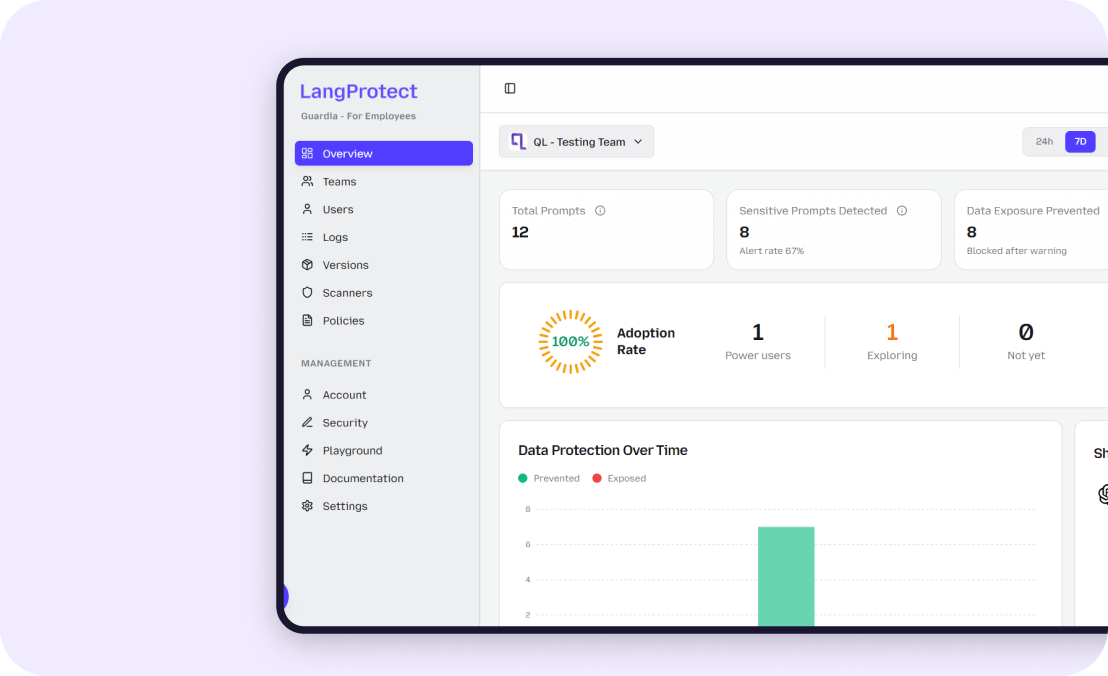

- The Action: Use Breachers Red and Guardia’s logging engine to maintain a 100% "interaction ledger."

- The Win: You move from periodic sampling to Continuous Monitoring. By maintaining a cryptographically secured log of not just the "answer," but the AI’s internal thought process, you ensure you are always ready for a SOX audit or a GDPR DSAR request.

Fintech Leadership Summary

In 2026, AI resilience is a competitive moat. If you can prove to your investors, auditors, and customers that your AI is Managed, Governed, and Defensible, you secure your license to lead.

Stop treating AI as a "risk to be avoided." Use LangProtect to turn your Shadow AI liabilities into governed strategic assets.

Don’t Wait for the Audit—Be Audit-Ready.

Whether you are securing the payment pipeline for **PCI DSS 4.0 **or hardening your internal lending agents, LangProtect provides the only interaction-aware security stack built for high-stakes finance.